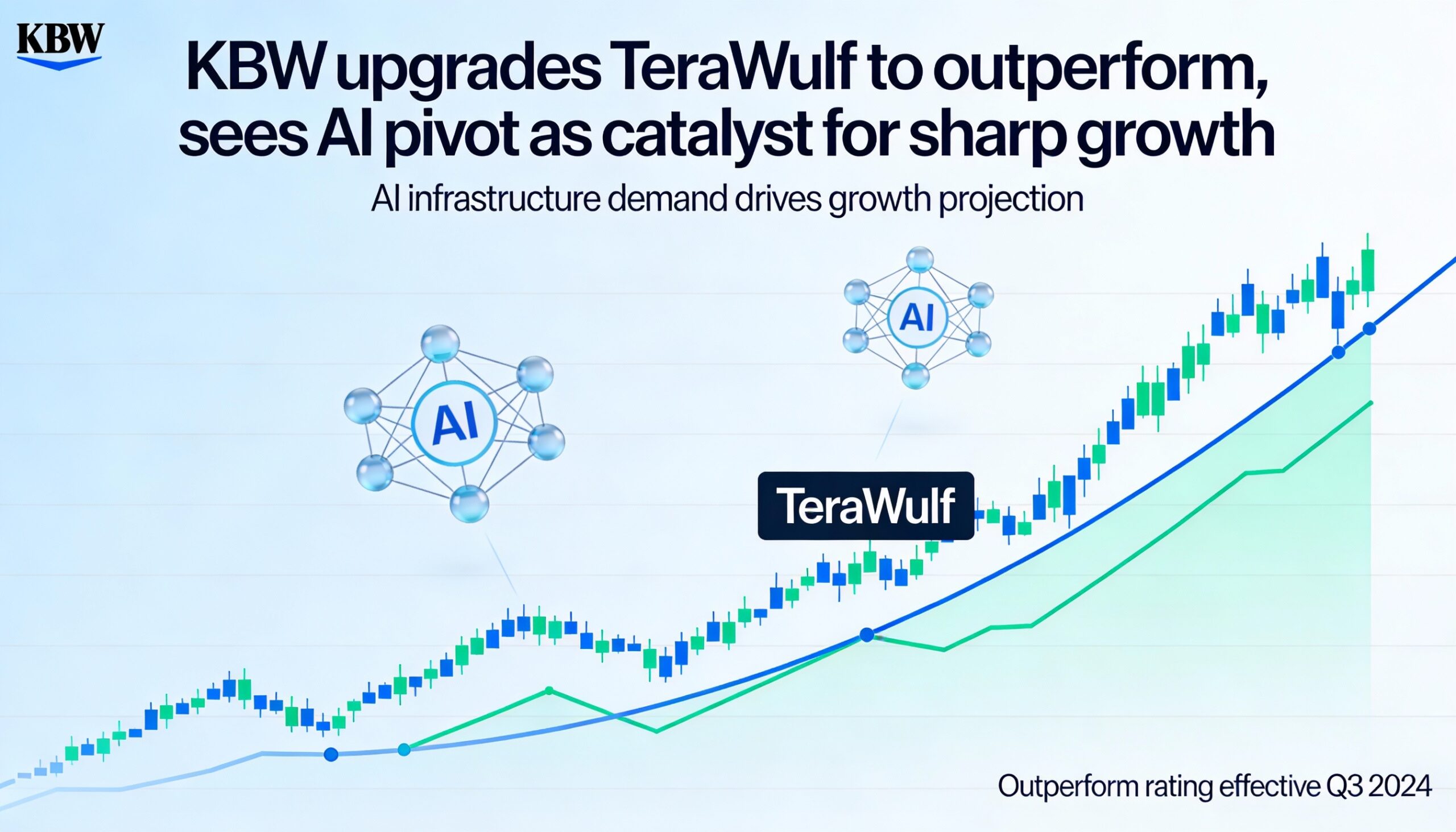

KBW upgraded TeraWulf (WULF) to “outperform” from “market perform” and raised its price target to $24 from $9.50, citing the company’s shift from bitcoin mining to AI and high-performance computing (HPC) leasing as a key growth driver.

The bank said investors are underestimating the earnings potential from TeraWulf’s strategic pivot. Analyst Stephen Glagola wrote Wednesday, “Investors underappreciate the magnitude of the BTC mining to HPC leasing mix shift in 2026–2027 and robust growth catalysts on 646 MW net of visible HPC leasing pipeline through 2027.”

Shares were up modestly at $11.18 in early trading. The upgrade reflects a broader trend of bitcoin miners repurposing data centers to host AI and HPC infrastructure, improving profitability as traditional mining declines.

Glagola projects TeraWulf’s existing HPC leases could drive a 505% EBITDA CAGR from 2025 to 2027, supporting potential multiple expansion from the current 13.8x EV/EBITDA valuation. HPC leasing is expected to generate roughly two-thirds of revenue in 2026 and the majority of contribution profit, while mining becomes largely immaterial by 2027.

The report noted execution risks are lower than many assume, highlighting secured financing, a track record of delivery, and supportive debt markets. KBW said recent share weakness largely reflects sector-wide selling rather than company fundamentals and expects discounts to narrow as lease revenues scale, with additional upside from new HPC deals in the coming year.