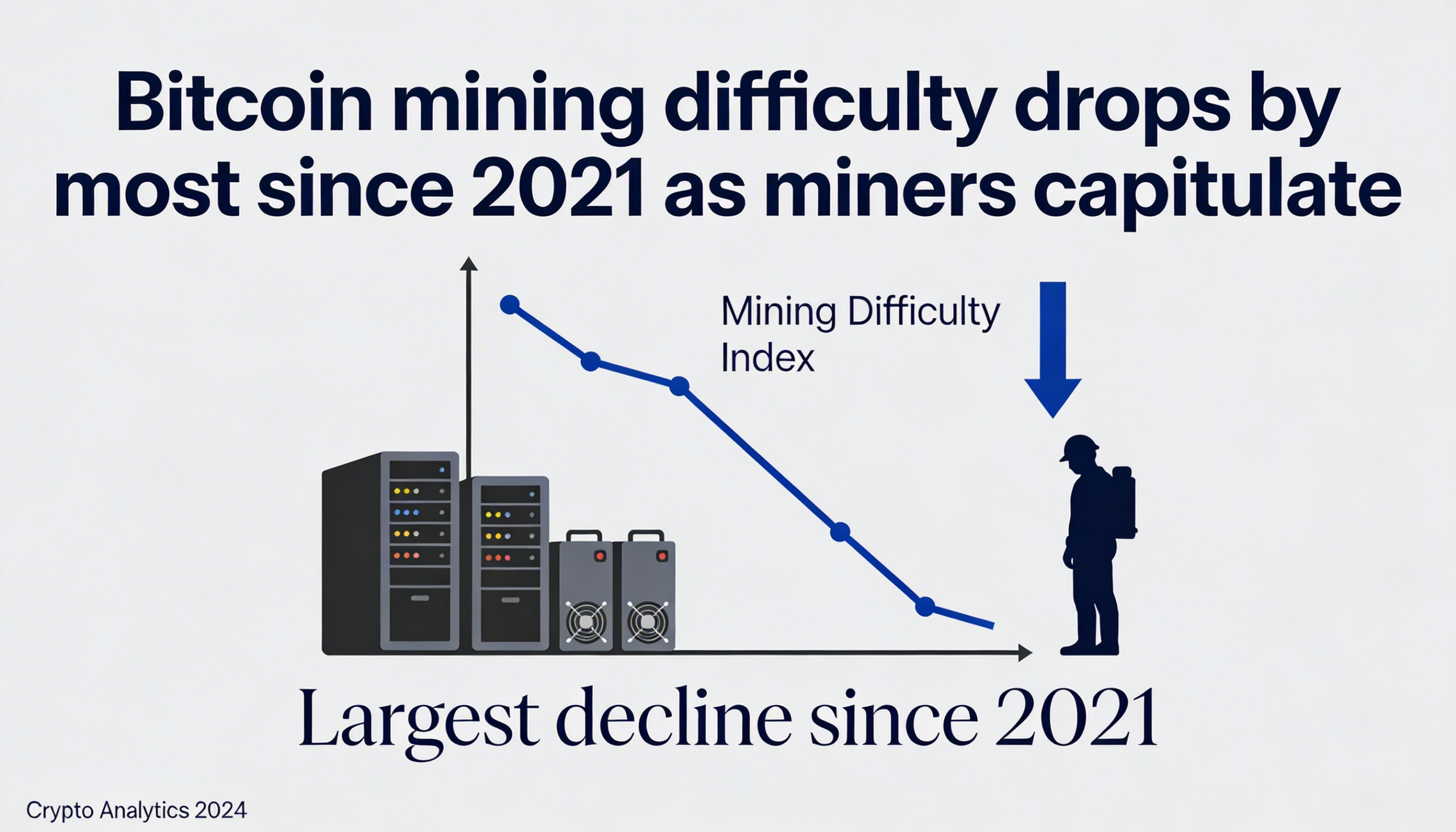

Bitcoin mining difficulty recorded its steepest drop since China’s 2021 crackdown, falling by about 11% in the latest adjustment as falling prices and winter storm–related power outages in the U.S. pushed miners offline.

The adjustment lowered difficulty from more than 141.6 trillion to roughly 125.86 trillion, according to Blockchain.com. Mining difficulty resets about every two weeks to maintain Bitcoin’s target block time of around 10 minutes.

The decline reflects growing stress across the mining sector. Bitcoin has fallen sharply from its October all-time high of $126,000 to roughly $69,500, eroding profitability. Mining revenue per unit of computing power has been hit particularly hard, with revenue per petahash dropping from around $70 at the peak to about $35.

Lower prices have forced many miners—especially those running older equipment or facing high electricity costs—to shut down machines. Some have redirected capacity toward artificial intelligence workloads, where large technology firms offer longer-term contracts and more stable returns.

Bitfarms said it is pivoting away from bitcoin mining toward data center development for high-performance computing and AI, a move that sparked a rally in the company’s shares.

Severe winter storms, particularly in Texas, compounded the pressure. Grid operators issued curtailment requests to prioritize residential electricity demand, leading public mining companies to scale back production. Some reported daily bitcoin output declines of more than 60%.

While sharp drops in mining difficulty can appear concerning, the mechanism is designed to be self-correcting. For miners that remain online, reduced competition can improve margins and help sustain operations.

Historically, major difficulty declines have coincided with periods of miner capitulation and have often preceded price stabilization or rebounds as miners sell bitcoin to cover operating costs.