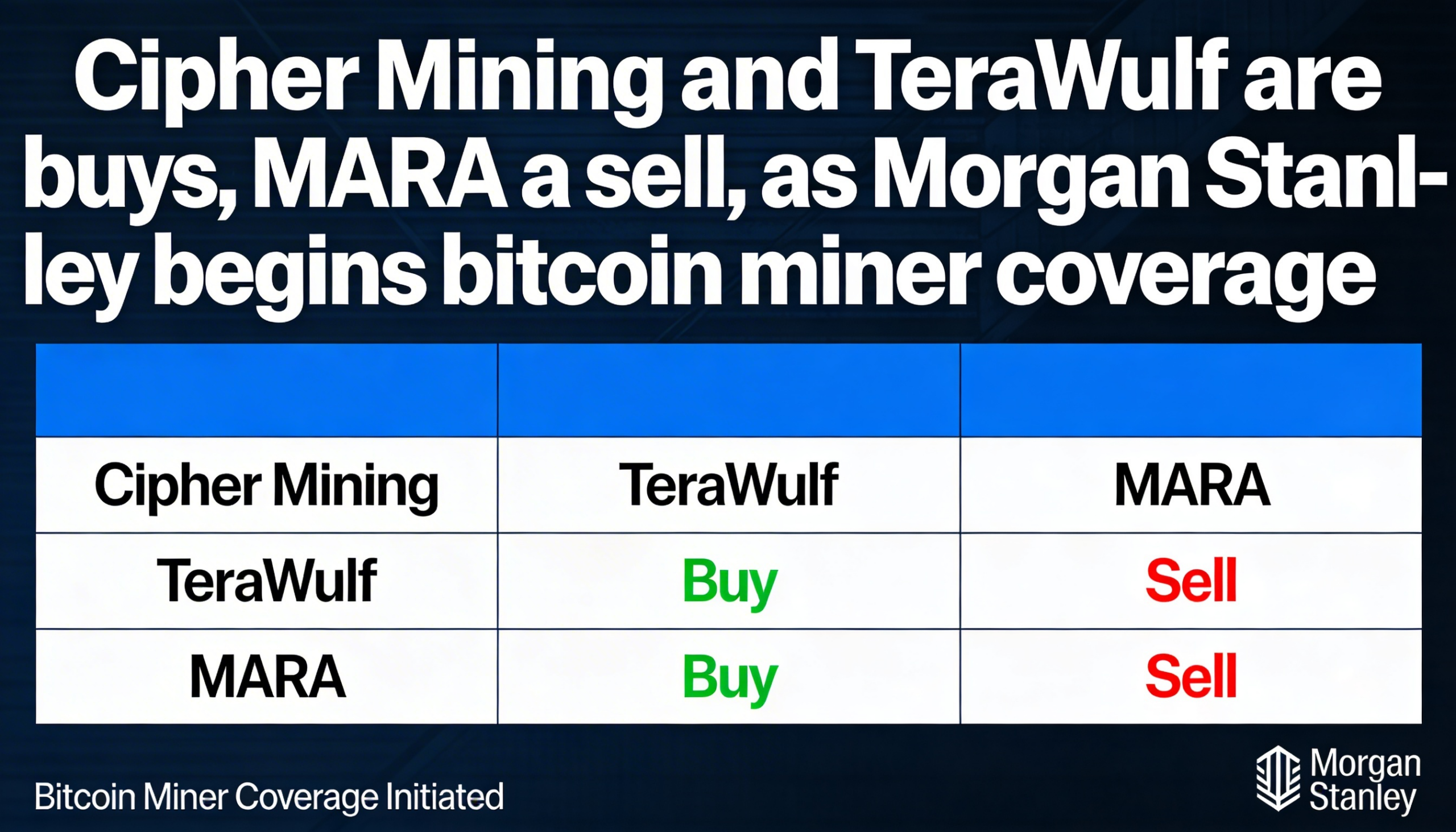

Morgan Stanley Initiates on Bitcoin Miners, Sees Greater Value in Infrastructure-Focused Names

Morgan Stanley began coverage of three publicly traded bitcoin miners on Monday, favoring companies positioned to monetize data center infrastructure while expressing caution on a miner more closely tied to bitcoin price exposure.

Analyst Stephen Byrd initiated Cipher Mining (CIFR) and TeraWulf (WULF) at Overweight, setting price targets of $38 and $37, respectively. Both stocks rallied following the report, with Cipher gaining 12.4% to $16.51 and TeraWulf climbing 12.8% to $16.12.

Marathon Digital (MARA) was launched at Underweight with an $8 price target. Shares were modestly higher at $8.28.

Morgan Stanley’s investment case hinges on the idea that certain mining sites can transition from volatile crypto operations into contracted infrastructure assets. Once facilities are supported by long-term leases with creditworthy counterparties, Byrd argues they should be valued based on stable, recurring cash flows rather than bitcoin’s price fluctuations.

He pointed to data center REITs such as Equinix (EQIX) and Digital Realty (DLR) as valuation reference points. Those firms trade at more than 20 times forward EBITDA, reflecting predictable earnings and scale advantages. While single-site conversions by miners may not command comparable multiples, Morgan Stanley believes the market may be undervaluing the long-term cash flow potential of successfully leased facilities.

Cipher Mining best fits what Byrd described as a potential “REIT endgame.” A shift from self-mining to leasing capacity to hyperscale or enterprise customers could transform its assets into infrastructure-like investments with utility-style revenue streams.

TeraWulf received similar treatment. The bank highlighted its experience securing data center agreements and management’s background in developing power infrastructure. Byrd estimates uncontracted sites could convert at a present value of roughly $8 per watt. His base case assumes the company achieves about 50% of its targeted 250 megawatts of annual data center expansion between 2028 and 2032, with additional upside if execution reaches 75%.

Marathon Digital drew a more cautious assessment. Byrd noted that the company’s hybrid strategy — maintaining significant bitcoin mining while pursuing data center initiatives — limits its potential for infrastructure-style rerating. MARA’s continued emphasis on accumulating bitcoin, including through convertible debt issuance, leaves its valuation primarily tied to mining economics.

Morgan Stanley also highlighted structural risks within the mining industry, citing historically weak returns on invested capital. For Marathon, mining profitability remains the principal driver of equity performance.

The initiation reflects a broader reassessment across the sector as miners explore shifting from pure crypto exposure to power and computing infrastructure. Morgan Stanley’s stance is selective: companies able to secure long-term, contracted data center revenue may justify higher valuations, while those reliant on bitcoin price dynamics face a more constrained path forward