A surge in activity at lower strike prices is pointing to rising demand for downside protection in bitcoin following its sharp drawdown.

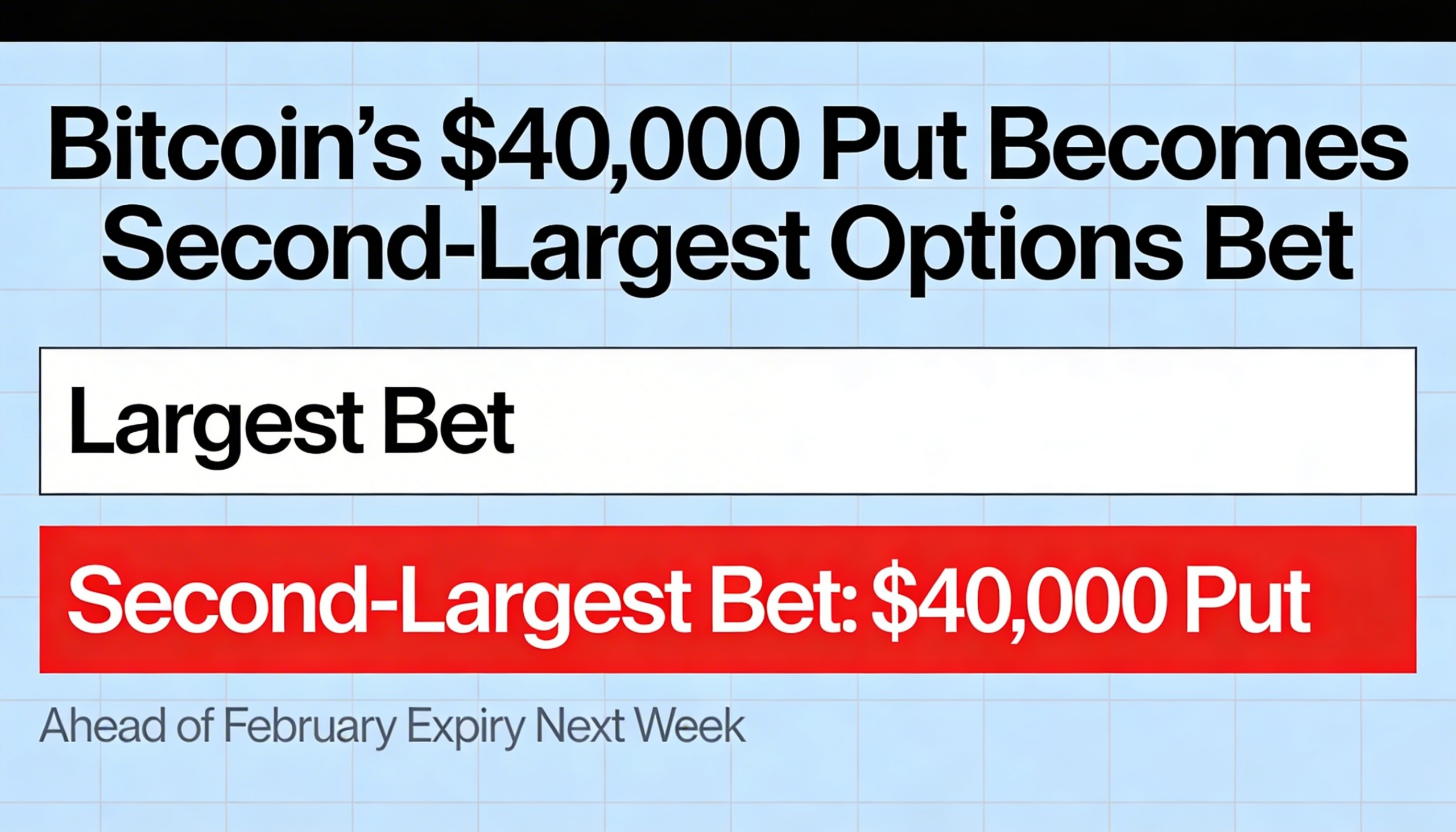

The $40,000 put option has become one of the most concentrated positions ahead of the Feb. 27 expiry, signaling that traders are actively hedging against the possibility of further losses. Put options give holders the right, but not the obligation, to sell bitcoin at a predetermined price before expiration, effectively serving as insurance if prices fall below the strike.

With roughly $490 million in notional open interest, the $40,000 strike is now the second-largest concentration in the market. The scale of that positioning highlights appetite for tail-risk protection. Bitcoin has dropped as much as 50% from its October peak and is currently trading near $66,000, prompting a broad adjustment in derivatives exposure as participants guard against renewed downside.

Data from Deribit — the Dubai-based options exchange owned by Coinbase — shows that around $7.3 billion in bitcoin options notional value is due to expire at month-end.

Meanwhile, about $566 million in open interest is concentrated at the $75,000 strike, which also marks the “max pain” level — the price at which the largest number of options contracts would expire worthless, minimizing payouts to buyers. With bitcoin trading below $75,000, a move higher into expiry could help reduce losses for call sellers.

Although call contracts still exceed puts overall — 63,547 calls versus 45,914 puts — positioning is not decisively bullish. The put-to-call ratio of 0.72 suggests upside bets remain dominant, yet the heavy buildup of put open interest at lower strikes underscores meaningful demand for downside insurance.

In essence, traders are keeping exposure to a potential recovery while simultaneously bracing for the risk of another sharp leg lower.