Here’s a fresh rewrite with a tighter, more streamlined tone:

The Senate passed a nonbinding resolution without objection after Sam Bankman-Fried sought clemency, coming months after former President Donald Trump granted pardons to several prominent crypto figures, including Changpeng Zhao and Ross Ulbricht.

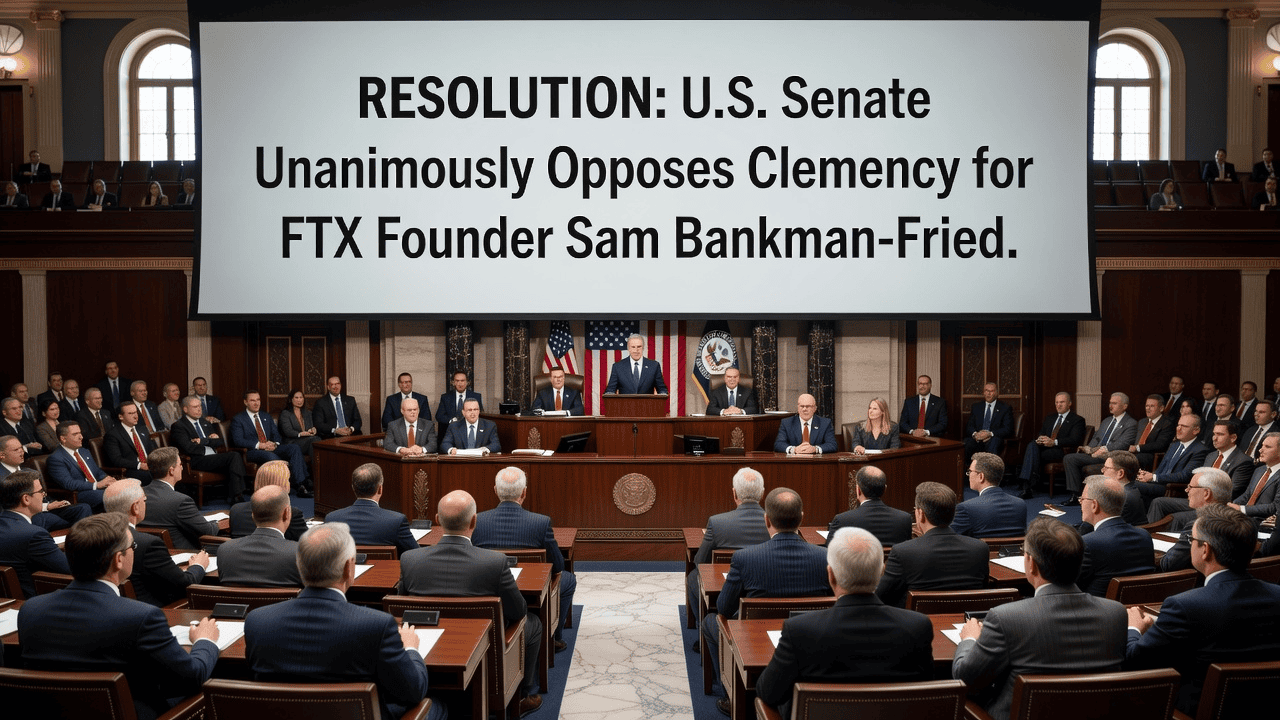

On Wednesday, lawmakers made clear that the FTX founder should never receive leniency, approving a measure stating he should not be granted a pardon or sentence reduction under any circumstances.

The resolution was adopted through unanimous consent, a process that allows a measure to pass as long as no senator objects.

It was led by Senators Cynthia Lummis, a Wyoming Republican, and Ruben Gallego, an Arizona Democrat, the top Republican and Democrat on the Senate Banking Committee’s digital assets subcommittee.

Lummis, a leading advocate for the crypto industry in Congress, has spent years advancing related legislation while also pushing to ensure one of its most high-profile figures remains imprisoned.

“He had his day in court,” Lummis said when introducing the resolution on June 17. Gallego echoed the sentiment more bluntly: “Keep him locked up.”

Bankman-Fried is not expected to be eligible for release until around 2044. A jury convicted him in November 2023 on seven charges tied to FTX’s collapse — a case prosecutors described as one of the largest financial frauds in U.S. history, with more than $8 billion in losses suffered by American customers.

Earlier this year, Trump said he had no plans to pardon Bankman-Fried, despite having granted clemency to Binance founder Changpeng Zhao, Silk Road creator Ross Ulbricht, and other white-collar offenders.

Bankman-Fried ran both FTX and Alameda Research. FTX operated as a crypto exchange meant to safeguard customer funds, while Alameda was a trading firm he also owned. He redirected billions in customer deposits from FTX to Alameda, which used the money for trading, venture investments, political donations, and Bahamian real estate. Alameda also received special treatment within FTX’s system, allowing it to bypass safeguards that would have applied to other traders.

The operation began to unravel in November 2022 after CoinDesk obtained Alameda’s balance sheet, revealing that much of its reported assets consisted of FTT — a token created by FTX itself.

In effect, Alameda’s financial backing relied heavily on an asset issued by its sister company. The situation worsened when Binance announced it would sell its FTT holdings, triggering a sharp drop in the token’s price.

As confidence collapsed, customers rushed to withdraw their funds, but FTX could not meet the demand because the money was no longer available. The exchange filed for bankruptcy on Nov. 11, 2022, just over a week after the report surfaced.