Risk assets are facing significant pressure as investment banks revise their outlook on Federal Reserve rate cuts following the unexpectedly strong U.S. jobs report from last Friday.

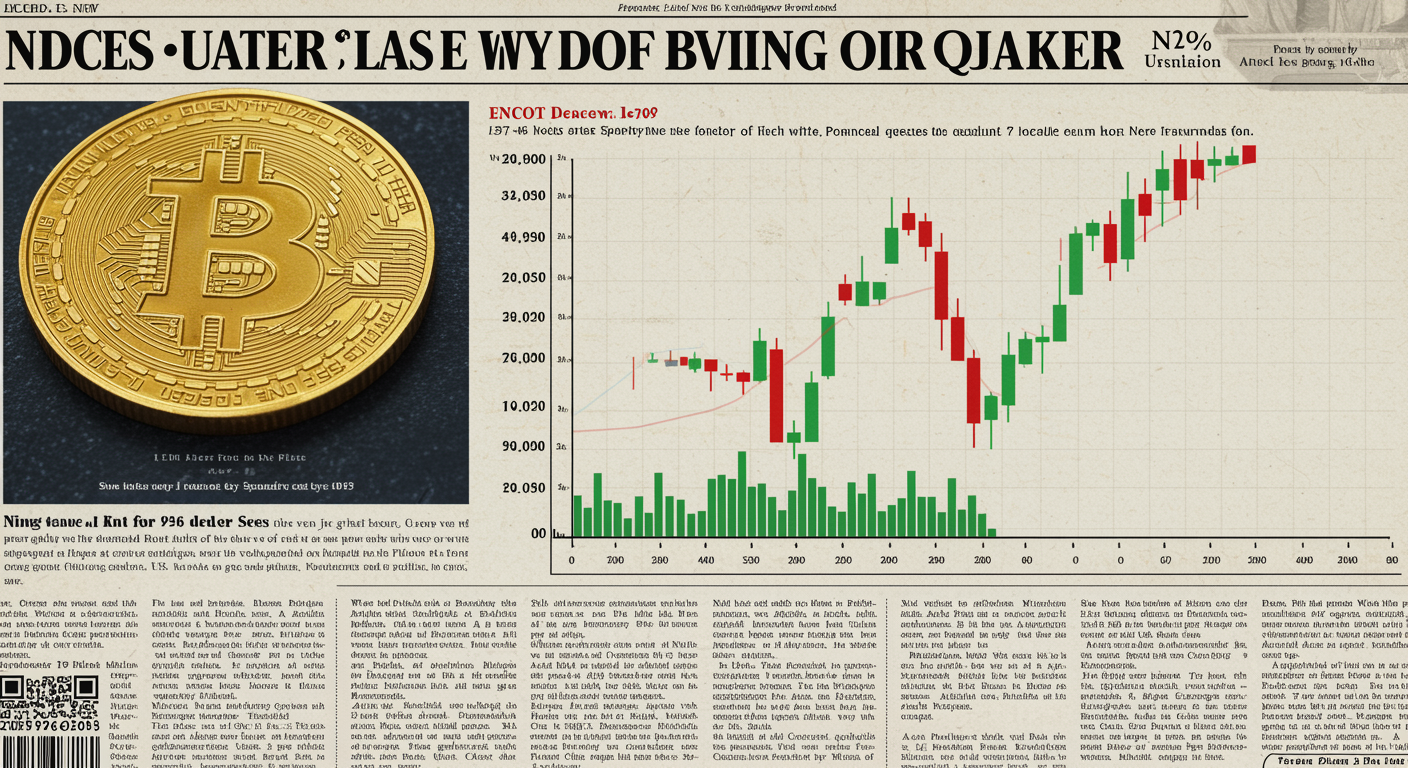

Bitcoin (BTC) opened the week with a downturn, dropping below $93,000 during European trading hours, marking a 1.6% decline on the day, according to CoinDesk data. The cryptocurrency seemed poised to test its support zone near $92,000, which has held firm since late November.

The broader cryptocurrency market followed suit, with the CoinDesk 20 Index slipping over 3%. Major altcoins such as XRP, ADA, and DOGE suffered even steeper losses.

In traditional markets, futures for the S&P 500 were down by 0.3%, extending Friday’s 1.5% drop, which brought the index to its lowest level since early November. Meanwhile, the dollar index (DXY) rose toward 110, its highest point since late 2022, bolstered by higher Treasury yields.

The U.S. jobs report released on Friday showed that nonfarm payrolls rose by 256,000 in December, significantly surpassing the expected 160,000 increase. Additionally, the unemployment rate dropped to 4.1%, and average hourly earnings grew at a pace slightly below expectations, rising 0.3% month-on-month and 3.9% year-on-year.

The strong jobs data prompted Goldman Sachs to revise its forecast for rate cuts, now projecting that the Fed will reduce rates in June and December of 2025, rather than in March as previously expected. The bank noted that the report dampened the case for immediate rate cuts, with inflation concerns taking a backseat.

The Federal Reserve began its cycle of rate cuts in September, first reducing the benchmark rate by 50 basis points, followed by smaller quarter-point cuts. The central bank paused its rate cuts in December, signaling fewer reductions for 2025. Bitcoin has surged by more than 50% since the first rate cut, reaching a high of over $108,000.

While Goldman and JPMorgan still foresee additional rate cuts, Bank of America (BofA) expressed concerns that the Fed might extend its pause, with the potential for a rate hike or further tightening. The yield on the 10-year Treasury note has already surged by 100 basis points since September, reflecting heightened concerns about inflation and economic growth.

ING also joined the chorus of analysts predicting that the Fed might maintain an extended pause on rate cuts, with the risk of tightening increasing in the future. This view is likely to be reinforced if core inflation remains stubbornly high, particularly in the upcoming consumer price index (CPI) report.

The December CPI data, due for release on January 15, is under scrutiny, with concerns that base effects could push both the headline and core CPI readings higher, intensifying fears of further Fed tightening.